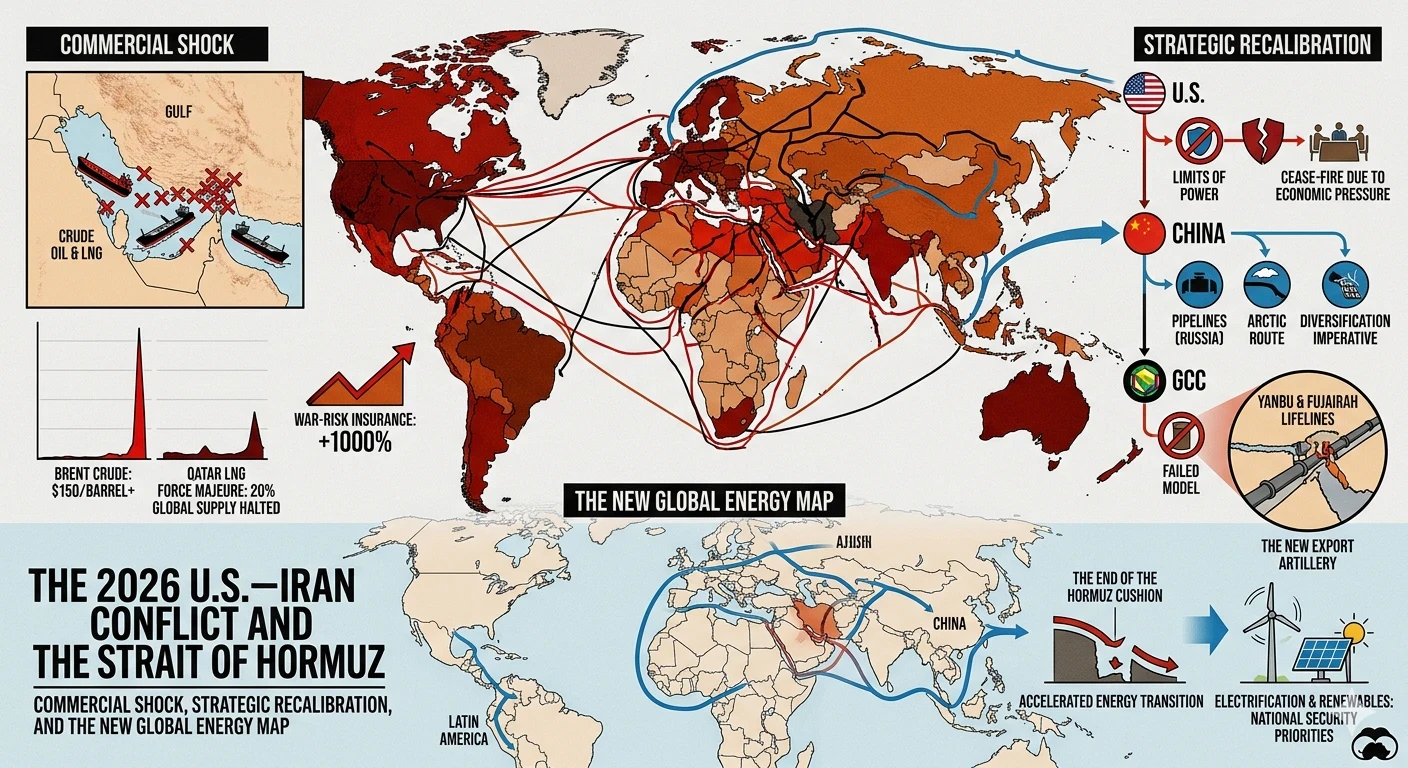

The 2026 U.S.–Iran Conflict and the Strait of Hormuz: Commercial Shock, Strategic Recalibration, and the New Global Energy Map

The Strait of Hormuz — a narrow maritime corridor between Oman and Iran linking the Persian Gulf to the Arabian Sea — has long been the world’s most consequential energy chokepoint. In 2026, direct conflict between the United States and Iran dramatically amplified that role, producing immediate shocks and catalyzing structural shifts in global commerce. For importers, exporters, shipowners, insurers and policy makers, the crisis turned standard contingency plans into urgent, expensive decisions. This article examines the commercial fallout: what happened to flows of crude oil, refined products and liquefied natural gas (LNG); how shipping and insurance markets reacted; which alternate routes and investments became commercially viable; and what the medium- to long-term implications are for global trade and energy security.

Immediate commercial impacts

- Disruption to oil and LNG flows Before 2026, roughly 20–30% of seaborne-traded crude oil and a significant share of global LNG transited the Strait of Hormuz. Military strikes, mine-laying, attacks on tankers, and heightened naval interdictions led many tankers to suspend transits or reroute. Immediate impacts included:

- Spot and futures price spikes: Brent and other benchmarks surged on fear-driven buying and physical tightness. Price volatility intensified as traders raced to book alternative cargoes.

- Cancelled or delayed cargoes: Some crude and LNG cargoes were rolled or canceled, creating short-term mismatches at refineries and regasification terminals.

- Curtailment by Gulf producers: Even producers intent on maintaining output reduced exports due to transportation risk, crew safety concerns, and insurance reluctance. This intensified downstream tightness.

- Shipping behavior and operational costs Shipowners responded rapidly to increased threat levels:

- Rerouting via the Cape of Good Hope: Many tankers chose the longer route around southern Africa. While safer from immediate conflict risks, the detour added 7–12 days (or more) and millions in extra voyage costs per ship, depending on cargo and vessel speed.

- Alternative routing through Iraq/Turkey pipelines: Where pipeline capacity and commercial agreements allowed, crude and refined traffic shifted to overland arteries such as the Iraq–Turkey export routes and the regional pipeline networks, albeit limited by capacity and political constraints.

- Crew and port call changes: Ships reduced port calls in higher-risk regional ports, extended ballast legs, and implemented higher-crew costs for security measures.

- Insurance, P&I and security premiums Insurance markets reacted sharply:

- War risk and kidnap & ransom premiums: P&I clubs, hull and machinery underwriters, and specialized war-risk markets imposed large surcharges or withdrew cover for transits in proximity to the Strait. For some routes, insurance costs climbed to levels that made voyages uneconomic.

- Security measures: Shipowners investing in armed security teams, hardened hulls, and rerouting incurred significant extra expenses. Some charterers refused to accept vessels equipped with armed guards or required higher indemnities.

- Freight and supply-chain contagion Beyond energy:

- Tanker freight indices spiked; time-charter rates rose for Aframax, Suezmax, VLCC segments as supply tightened and ballast distances increased.

- Non-energy bulk and container trade experienced knock-on effects as container vessels avoided near-region transits, increasing lead times and freight rates on certain lanes.

- Strategic commodities, scheduled shipments, and just-in-time supply chains suffered delays that rippled through manufacturing and retail sectors.

Commercial responses and adaptations

- Diversification of supply and demand-side adjustments

- Importers accelerated diversification: Buyers in East Asia and Europe accelerated contracting with non-Gulf suppliers (West Africa, Russia where feasible, US exports, South America) and increased purchases in spot markets to build inventories.

- Strategic reserves tapped: Countries with strategic petroleum reserves released stocks to stabilize markets, smoothing short-term supply gaps.

- Demand destruction: High prices and trade disruptions led to some demand destruction — fuel switching, delayed industrial activity, reduced discretionary transport — tempering price increases.

- Rerouting and infrastructure acceleration

- Investment surge in alternate routes: The crisis drove renewed urgency to expand pipeline capacity (Iraq–Turkey, UAE–Oman pipelines), increase storage capacity in strategic hubs (Fujairah, Jebel Ali, Rotterdam), and consider new transshipment and bunkering nodes outside the immediate conflict zone.

- Expand shipping around Africa: Shipowners and charters factored the Cape route into commercial war-gaming. Longer-term, increased vessel utilization and slower steaming reduced some incremental costs but lengthened cargo cycle times and fleet demand.

- LNG supply flexibility: Floating storage and regasification units (FSRUs) and spot LNG cargo trading helped some buyers manage disruptions. However, LNG supply chains — demanding specific carriers and regasification scheduling — were less flexible than crude oil.

- Insurance market innovations

- Layered risk-sharing: Where possible, governments and export credit agencies provided backstops or guarantees, reinsurers increased capacity, and specialized war-risk pools emerged to underwrite high-premium routes.

- Conditional coverage and corridor windows: Insurers developed short-duration corridor policies when diplomatic windows opened, allowing limited safe passage under naval escort conditions.

Economic and geopolitical knock-on effects

- Regional economies

- Gulf producers faced contradictory pressures: need to maintain revenue vs. limited export logistics. Those with diversified export infrastructure (e.g., UAE’s east-coast Fujairah terminals) fared relatively better than those dependent solely on Hormuz transit.

- Non-oil sectors (shipping services, bunkering, logistics hubs) in proximate states experienced steep short-term revenue declines as vessels avoided the region.

Global inflationary pressures Energy price spikes fed through higher transportation and production costs globally, contributing to inflation and central-bank policy dilemmas in import-dependent economies.

Strategic reorientation by energy importers

- Geographic rebalancing: Europe and Asia intensified long-term contracts with alternative producers, accelerated renewable transitions, and expanded strategic storage.

- Investment in resilience: Buyers prioritized supply-chain resilience over purely lowest-cost procurement — favoring flexible cargoes, diversified supplier portfolios, and longer-term security-of-supply contracts.

Longer-term structural changes

- Permanent shift in shipping economics and route planning Freight markets and chartering strategies adjust to the elevated probability of future disruptions:

- Built-in contingency costs become normalized in charter rates for Gulf-origin cargoes.

- New transshipment and storage hubs outside the Persian Gulf attract investment, gradually reshaping regional maritime geography.

Acceleration of energy transition Persistent risk premium on hydrocarbons sourced through conflict-prone chokepoints bolstered investment and policy momentum toward renewables, electrification, hydrogen, and local storage capacity. While this transition is uneven and capital-intensive, private and public-sector stakeholders increasingly factor geopolitical risk into long-term energy planning.

Increased regional infrastructure investment Governments and private consortia pursued projects to bypass chokepoints:

- Pipelines with higher throughput and security measures.

- East-coast terminals in Gulf states and alternate ports for direct exports to Asia (reducing the need to cross Hormuz).

- Investment in rail and trucking corridors where feasible to move crude and products to safer export terminals.

Policy, legal and operational considerations for commercial actors

Legal and contractual risk management Contracts (charters, sale and purchase agreements) were renegotiated to clarify force majeure triggers, safe port clauses, and allocation of increased voyage costs. Companies reassessed contractual exposure to war risk and indemnity allocation.

Private-sector contingency planning Shipowners, charterers, and commodity traders strengthened monitoring, crisis playbooks, and coordination with naval escorts and flag states. Many implemented real-time threat analysis and rerouting protocols.

Role of diplomacy and naval escorts Diplomatic channels and naval escorts (multi-national convoys) periodically opened safe windows, but escorts are costly and do not eliminate all risk. Commercial actors had to weigh the trade-off between transit speed and escort availability.

Outlook and recommendations

- For importers and traders

- Diversify supply sources and contracts; secure flexible cargo terms.

- Increase elastic storage capacity to buffer supply shocks.

- Factor higher insurance and freight premiums into supply-cost models.

- For shipowners and insurers

- Develop flexible operational models that can switch between high-risk, short-route economics and low-risk, long-route economics.

- Collaborate with reinsurers, governments and PSCs (private security companies) to design affordable, scalable war-risk coverage.

- For governments and regional authorities

- Expedite investment in alternative export infrastructure and crisis-ready storage.

- Coordinate internationally to provide insurance backstops or limited guarantees to sustain critical flows without rewarding aggression.

- Use diplomacy to reduce escalation and keep commercial corridors open where possible.

The 2026 U.S.–Iran conflict transformed the Strait of Hormuz from a chronic geopolitical risk into an acute commercial crisis. The immediate effects — elevated oil and LNG prices, disrupted shipping, and spiking insurance costs — were severe, but equally important are the structural adjustments now under way: rerouting economics, accelerated infrastructure investment, diversified supply chains, and an implicit premium on geopolitical resilience. For private-sector actors, the crisis has underscored the need to internalize geopolitical risk into commercial decision-making. For states, it has highlighted the strategic urgency of creating redundant export routes and supporting market instruments that can dampen shocks without encouraging instability. The Strait of Hormuz remains a single point whose disruption reverberates globally; the 2026 conflict has likely made the world a littler less dependent on it — but also reminded every player that diversifying energy and logistics pathways is not optional but commercially essential.